{kind=link}

A Guide to a Financial Services Marketing Agency in 2026

Hiring a financial services marketing agency? This guide explains core services, compliance, KPIs, and how to select a partner for the AI-driven era.

Subtitle: Financial marketing no longer wins by saying more. It wins by making every claim legible to regulators, customers, and machines.

Date: June, 2026

The category has already changed. A financial services marketing agency now operates as a system for producing verifiable truth, not a vendor that ships campaigns.

Regulatory review is constant. Customer expectations for relevance are high. AI systems now mediate discovery, summarization, and comparison. Those three conditions change the agency mandate. The work is no longer limited to attracting attention. It includes structuring claims, evidence, disclosures, and entity relationships so they can survive review by compliance teams, scrutiny from buyers, and retrieval by machine systems.

That requirement breaks the legacy buying model. Service menus such as SEO, paid media, creative, and web design describe production capacity, but they do not reveal whether an agency can make financial information dependable across channels and interpreters. In this category, the harder problem is informational integrity. Can the agency turn product claims into traceable, approved, machine-readable assets? Can it preserve meaning as those assets move from webpage to ad unit to AI-generated answer?

Large language models make this standard visible. They infer authority from consistency, citation structure, entity clarity, and document-level coherence. A brand can publish accurate material and still lose retrieval if its information is fragmented, weakly sourced, or semantically inconsistent. In financial services, that failure has direct cost. It slows approval cycles, reduces discoverability, and increases the odds that customers or machine systems misread the offer.

The modern financial services marketing agency should therefore be evaluated as an information engineering partner. The output consists of claims that are reliable for humans, verifiable by regulators, and interpretable by AI without distortion.

Table of Contents

Executive Summary A New Mandate for Verifiable Trust

The Trust-Compliance Matrix A Proprietary Framework

Why service menus mislead buyers

How the matrix works in practice

What buyers should demand

Deconstructing Core Services Through an AI Lens

The data layer comes first

Each service becomes a machine-readable signal

Why this changes agency design

The Measurement Paradigm Shift to Business Outcomes

Semantic Density replaces dashboard theater

What strong reporting looks like

The C-suite implication

Decoding Agency Pricing and Engagement Models

Cost signals competence in this category

Which model fits which mandate

The timeline mistake buyers keep making

How to Evaluate and Shortlist Agency Partners

Ask for operational proof

Use a reverse RFP to expose capability

What disqualifies an agency immediately

Conclusion The Future Is Verifiable

Authority becomes information architecture

Agency selection becomes a truth test

The strategic end state

Executive Summary A New Mandate for Verifiable Trust

A financial services marketing agency is no longer best understood as a campaign vendor. It is an information engineering function charged with making regulated claims legible, consistent, and verifiable across human and machine interpretation.

That change is structural.

Financial brands now operate under two review systems at once. Regulators assess whether communications are fair, balanced, and properly qualified. AI-mediated discovery systems assess whether the same communications are coherent, repeated consistently, and attached to an identifiable source. A firm can satisfy one system and still fail in market visibility if its knowledge is fragmented. It can also perform well in discovery and create avoidable exposure if its claims cannot be substantiated across channels.

The issue lies not only in creativity but in maintaining truth.

This is why the category has changed shape. Personalization pressure pushes firms toward relevance and specificity. Compliance pressure pushes them toward precision and evidence. AI search, answer engines, and retrieval systems intensify both demands because they rank and summarize what they can parse, reconcile, and cite. In practice, this means that a compliant statement with weak retrieval value underperforms, while a persuasive statement with weak evidentiary support creates risk.

A high-quality financial services marketing agency therefore works at the level beneath copy. It defines entities, normalizes claims, maps disclaimers to each distribution point, and preserves semantic consistency across websites, paid media, CRM workflows, advisor bios, product pages, and third-party citations. The output may look like content marketing or demand generation. The underlying job is closer to controlled knowledge architecture.

That standard invalidates the old agency checklist. Service inventories such as SEO, paid media, email, social, and web design describe production capacity. They do not show whether the agency can maintain claim integrity in a regulated environment or build content that machines can retrieve without distorting meaning.

A more serious evaluation starts with four questions:

Does the agency preserve claim consistency across the full content graph? Product details, risk disclosures, eligibility language, and supporting evidence must remain aligned in every public and operational system.

Does the agency publish expertise in machine-readable formats? Human-readable authority is no longer enough. The information must also be structured for search engines, answer engines, and retrieval workflows.

Does the agency support personalization with auditable data practices? Relevance depends on consent, identity logic, and data lineage that can withstand scrutiny.

Does the agency measure commercial outcomes instead of surface activity? Regulated buying cycles require reporting tied to qualified demand, progression, and revenue influence, not only clicks or sessions.

Algomizer treats this shift as a move from promotional marketing to verifiable trust engineering. The distinction matters because authority in financial services is increasingly inferred from information quality, not asserted through brand language alone.

The agencies that will matter in this category do three things repeatedly and at scale. They standardize evidence. They reduce ambiguity. They increase discoverability without weakening compliance.

That is the new mandate for verifiable trust.

The Trust-Compliance Matrix A Proprietary Framework

A financial services marketing agency should be judged by risk handling and truth legibility, not by service breadth. That requires a sharper model than the standard agency capabilities slide.

Why service menus mislead buyers

Agency websites usually describe channels. SEO, PPC, content, social, web, analytics. That taxonomy hides the actual operating problem.

In financial services, the buying decision focuses on the agency's ability to shift an activity into a zone that fosters trust while avoiding compliance exposure. Existing industry commentary makes the gap explicit. Select Advisors Institute's perspective on financial services marketing agencies argues that buyers should demand evidence of category-specific measurement, including compliance review workflow, attribution methods, and reporting tied to qualified opportunities rather than clicks or traffic.

That requirement leads to a better framework. Algomizer defines it as the Trust-Compliance Matrix.

How the matrix works in practice

The matrix has two axes.

Axis | Low end | High end | What it tests |

|---|---|---|---|

Trust | Weak credibility, thin explanation, low proof | Strong authority, clear evidence, stable claims | Whether buyers and machines can rely on the information |

Compliance | Informal review, inconsistent controls | Formal review, approved language, governed distribution | Whether the activity can survive scrutiny |

This creates four operational states.

Quadrant | Condition | Typical failure |

|---|---|---|

Risk Zone | Low trust, low compliance | Fast production of content or ads that create exposure and little authority |

Ethical Tightrope | High trust, low compliance | Persuasive messaging that drifts beyond approved claims |

Bureaucratic Barrier | Low trust, high compliance | Safe language that no buyer remembers and no model retrieves confidently |

Growth Engine | High trust, high compliance | Evidence-rich communication with controlled approvals and measurable outcomes |

The focus is on directing efforts toward the Growth Engine quadrant.

Practical rule: If an agency can't explain how an asset moves from draft to approved, attributed, and reusable evidence, it doesn't control the quadrant it claims to operate in.

A new ad campaign often begins in a high-risk state because copy variation, audience targeting, landing page promises, and disclosures can diverge quickly. A detailed educational page can begin with stronger trust potential, but only if it ties claims to a stable evidence base and approved terminology. The matrix reveals why "content" and "paid media" aren't strategic categories by themselves. Execution quality depends on governance and verifiability.

What buyers should demand

A shortlist should be built around operational proof, not pitch polish. The useful questions are narrower than most procurement teams ask.

Show the review path. The agency should map draft creation, legal review, revision control, and final publishing authority.

Show the attribution path. The agency should connect published assets to qualified opportunities, not just session volume.

Show the evidence path. The agency should demonstrate how core claims are stored, reused, and checked across channels.

That standard disqualifies many firms immediately. It also clarifies what a real financial services marketing agency is. It is a trust system with campaign execution attached.

Deconstructing Core Services Through an AI Lens

Core services don't disappear in the AI era. They change function. Each becomes a signal system that shapes how models retrieve, rank, and restate a financial brand.

The data layer comes first

A financial services marketing agency can't personalize or attribute reliably without data unification. Alkami's marketing automation guidance for financial institutions is direct on this point: data aggregation and standardization come first, and a feedback loop is required to measure performance and improve campaigns over time.

That means first-party transaction data, CRM records, and external inputs need a shared identity framework before activation. Without that layer, the same customer appears as multiple entities across systems. Segmentation breaks. Journey analysis breaks. Machine learning models inherit fragmented labels and produce misleading recommendations.

This is also where governance enters the stack. Teams evaluating AI policy often review external references on model oversight and operating controls, such as this visual resource on AI governance solutions from Freeform Company. The relevance is straightforward. In finance, uncontrolled AI inputs create uncontrolled outputs.

Each service becomes a machine-readable signal

A conventional service list misses what these functions do inside AI-mediated discovery.

Brand. A brand functions as an entity-resolution layer, providing naming consistency, product clarity, executive attribution, and a stable vocabulary. These repeated markers help models determine if separate documents refer to the same organization.

Website and app experience. Digital presence extends beyond UX, serving as a canonical source environment. Product pages, disclosures, FAQs, calculators, support pages, and documentation should consistently adhere to one approved meaning system. Aligning these elements enhances both conversion confidence and retrieval confidence.

Content marketing. Content should be regarded as Evidence Clusters. An Evidence Cluster consists of a collection of supporting assets that collectively elucidate a significant financial concept. These

Paid media. Paid distribution is often discussed as demand capture. In practice, it also tests message integrity. Ad variants reveal where user intent, regulated language, and landing-page evidence do or don't align. The value lies in identifying the claims that can endure both attention and scrutiny, not merely in acquiring traffic.

CRM and automation. Content should be regarded as Evidence Clusters. An Evidence Cluster consists of a collection of supporting assets that collectively elucidate a significant financial concept. These assets are specific enough to

A useful framing for teams adapting content and architecture to answer engines is AI search engine optimization. The concept matters here because financial content must be engineered for retrieval quality, not just indexed presence.

The machine doesn't "understand" trust the way a customer does. It approximates trust from consistency, repetition, source quality, and conflict reduction.

Why this changes agency design

A serious financial services marketing agency needs strategists, compliance-aware editors, lifecycle operators, analysts, and technical implementers working from one source of truth. Fragmented specialist vendors usually fail because each optimizes a local metric. One team drives clicks. Another team protects language. Another team manages CRM logic. No one owns the evidence graph across all three.

That fragmentation is exactly what LLM environments punish. When one product promise appears five different ways across the web, the model's confidence declines. When the claim is consistent, supported, and repeated in multiple approved formats, the model can retrieve it more reliably.

The implication is mechanical. The agency focuses on maintaining information integrity while operating at a large scale.

The Measurement Paradigm Shift to Business Outcomes

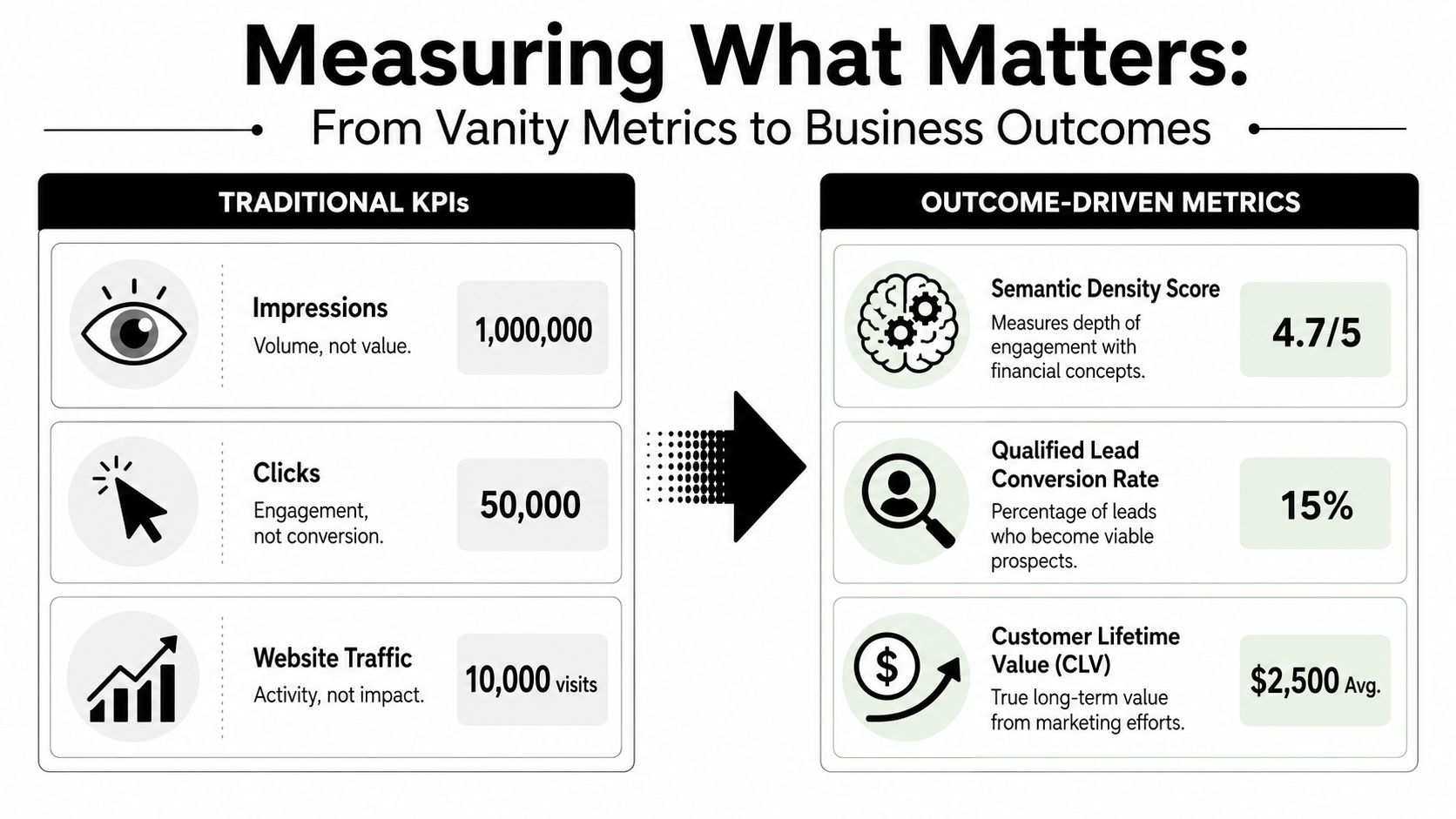

Financial marketing should report business events with high semantic content, not dashboard activity. That is the difference between observation and proof.

Semantic Density replaces dashboard theater

Algomizer defines Semantic Density as the amount of business-critical meaning contained in a metric. A metric with low semantic density tells a team that something happened. A metric with high semantic density tells the team whether that event mattered commercially and operationally.

A click is low density. It records motion. It says almost nothing about suitability, compliance alignment, downstream qualification, or revenue potential.

A completed application is high density. It sits closer to the regulated purchase cycle. It carries more operational meaning. It can be reconciled against funnel quality, onboarding success, and long-term account value.

Twilio's financial services marketing guidance makes this distinction explicit. The most effective measurement focuses on business-outcome metrics tied to the regulated purchase cycle, including applications started and completed, activation rates, customer lifetime value, and default-rate reduction.

What strong reporting looks like

A strong financial services marketing agency reports in layers.

Reporting layer | Low-density example | High-density alternative |

|---|---|---|

Attention | Impressions | Audience segments that progressed into approved funnel stages |

Engagement | Click-through rate | Applications started by approved audience cohort |

Conversion | Form submissions | Applications completed and activated |

Value | Cost per lead | Customer lifetime value by compliant acquisition path |

This doesn't mean clicks are useless. It means they are insufficient. They belong in diagnostic reporting, not executive reporting.

A dashboard that stops at traffic asks the wrong question. Financial firms need reporting that asks whether the campaign produced a qualified, compliant business event.

The practical consequence is that finance marketers should dismantle inherited KPI stacks when those stacks hide meaning. Executive teams don't need more top-of-funnel abstraction. They need spend tied to accountable outcomes.

A useful implementation path is to redesign dashboards around decision points rather than channels. Teams building reporting systems often benefit from examples of customizable SEO dashboards because the same principle applies here. The dashboard should reflect the decision architecture of the business, not the default output of an analytics tool.

The C-suite implication

This measurement model changes how marketing is funded internally. Once reporting connects spend to applications, activation, lifetime value, and risk-sensitive quality indicators, marketing stops looking like a discretionary awareness function. It becomes part of revenue operations and governance.

That shift also changes what an agency must prove. It isn't enough to generate interest. The agency must show that its work increased the volume of outcomes the business can bank.

Decoding Agency Pricing and Engagement Models

Financial services marketing agencies charge premium rates due to the high costs and compliance requirements in their environment. The pricing reflects the complexity of their work.

Cost signals competence in this category

A useful market anchor exists. According to Chatter Buzz's 2026 guide to financial services marketing agencies, competent firms commonly charge $8,000 to $25,000+ per month on retainer, $10,000 to $75,000+ per project, and $15,000 to $35,000+ per month for fractional CMO plus execution support. The same guide states that paid media usually produces initial performance data in 30 to 60 days, while SEO and content marketing often need 4 to 8 months to generate meaningful organic traffic and leads. Full ROI measurement in financial services often requires 6 to 12 months because sales cycles are longer.

These ranges matter because many procurement teams still compare specialized agencies to generalist shops. That comparison usually fails to account for legal review coordination, claim management, data engineering, and regulated attribution.

Cheap execution often shifts cost rather than reducing it. The invoice may look smaller. The rework burden grows.

Which model fits which mandate

The key consideration is not the cost of the model, but rather how well it aligns with the organization's decision speed, internal maturity, and evidence requirements.

Financial Services Marketing Agency Engagement Model Comparison

Model | Typical Monthly Cost | Best For | Key Feature |

|---|---|---|---|

Retainer | $8,000 to $25,000+ per month | Ongoing multichannel programs with continuous optimization | Persistent strategic and execution capacity |

Project-based | Varies, with projects commonly $10,000 to $75,000+ | Site launches, campaign builds, messaging overhauls, audits | Defined scope and contained deliverables |

Fractional support | $15,000 to $35,000+ per month | Teams needing senior strategy plus execution oversight | Embedded leadership without full-time executive hiring |

A retainer works when the company needs a standing operating layer. That usually includes paid media, content governance, lifecycle programs, and analytics that need constant calibration.

Project work fits bounded needs. A compliance-safe site rebuild, messaging architecture refresh, or content system redesign can often be structured cleanly as a scoped engagement.

Fractional support is suitable for companies with internal marketers requiring senior-level coordination. This model is effective when the issue lies in decision quality rather than labor capacity.

The timeline mistake buyers keep making

The most common budgeting error is expecting one timeline from every channel. Paid media can signal quickly. Organic systems usually can't. A board or leadership team that treats both the same creates pressure for premature judgment.

That is why engagement terms and reporting expectations should be aligned before kickoff. If a team hires for content authority and judges success on a short paid-media clock, it will likely kill the program before it matures. If it hires for rapid acquisition and waits on long-cycle reporting alone, it will miss key early diagnostics.

Price, model, and timeline must fit the information problem being solved.

How to Evaluate and Shortlist Agency Partners

Most firms still shortlist agencies by deck quality and client logos. That process selects for sales fluency. It does not select for compliance control, machine-readable content design, or outcome attribution.

Ask for operational proof

A serious financial services marketing agency should answer technical and procedural questions without hand-waving. The useful test is whether the agency can explain how it turns regulated knowledge into repeatable market signals.

The first pass should include questions like these:

Walk through the compliance workflow. Ask who drafts, who reviews, how revisions are tracked, and how approved language is stored for reuse.

Explain the information model. Ask how the agency structures claims, FAQs, proof points, and supporting assets so they remain consistent across channels and retrievable by AI systems.

Define the data prerequisites. Ask what customer and CRM inputs must be unified before personalization or automation starts.

Show the reporting logic. Ask how the agency connects campaigns to qualified opportunities, applications, activation, or lifetime value.

Describe AI usage constraints. Ask where AI is used in research, drafting, segmentation, and QA, and where human controls intervene.

Name the working team. Ask which strategist, analyst, editor, automation lead, and technical owner will operate the account.

A useful external primer for teams sharpening their measurement standards is this guide to hiring a marketing analytics agency. The overlap is practical. Analytics competence is one of the fastest ways to separate category operators from presentation-heavy vendors.

Use a reverse RFP to expose capability

A normal RFP lets agencies mirror the buyer's language and hide weak operating depth. A reverse RFP works better. Instead of asking for generic proposals, the buyer submits a narrow prompt that forces the agency to reveal its system.

A concise reverse RFP can ask for:

Prompt | What it reveals |

|---|---|

Map the review path for one regulated landing page | Compliance maturity |

Define the core business outcomes you would measure in the first reporting model | Metric quality |

Describe how one product claim would stay consistent across paid, organic, CRM, and off-site content | Information governance |

Identify the data dependencies for personalization | Technical realism |

Explain how the agency prepares content for AI-mediated discovery | GEO and AEO sophistication |

For teams specifically evaluating partners in AI-discovery environments, this guide on choosing your SEO AI agency provides a compatible screening lens.

A short video can also help internal stakeholders calibrate what modern vetting should look like before agency interviews begin.

What disqualifies an agency immediately

Several responses should end the conversation.

An agency that focuses on impressions over applications, emphasizes AI over governance, or mentions trust without demonstrating review controls is not prepared for financial services work.

Other immediate disqualifiers include vague attribution language, no explanation of approval pathways, channel teams working from separate source documents, and performance reporting that treats lead volume as the terminal goal.

A shortlist should be small. In this category, a smaller shortlist usually means a smarter one.

Conclusion The Future Is Verifiable

The future financial brand isn't the loudest publisher. It is the cleanest source system. That is why the role of a financial services marketing agency has changed so sharply.

Authority becomes information architecture

The old model rewarded reach. The new model rewards structured truth. Regulators demand clarity. Customers demand relevance. AI systems reward consistency, stable entities, and citable claims.

Those pressures don't conflict when the underlying information system is strong. They reinforce each other. A well-structured financial brand becomes easier to approve, easier to personalize, easier to retrieve, and easier to trust.

This is the hidden strategic shift. Marketing has moved closer to knowledge management and machine interpretation. Content is no longer just persuasion. It is a retrieval surface. Messaging is no longer just positioning. It is a claim taxonomy. Reporting is no longer just campaign summary. It is proof of business impact.

Agency selection becomes a truth test

That reframes procurement. The firm is selecting an operating partner to engineer verifiable truth under scrutiny, rather than hiring an outside team to produce assets.

The strongest partner will show four capabilities clearly:

Governance discipline. Review paths, approved language systems, and controlled publishing workflows.

Data integrity. Unified customer records that make personalization and attribution believable.

Evidence design. Content and digital assets built as reusable proof, not isolated creative units.

Outcome measurement. Reporting tied to business events that matter in regulated purchase cycles.

One practical option in AI-discovery work is Algomizer, which focuses on AEO, GEO, and AI search visibility across answer engines by shaping how brands are perceived, cited, and retrieved in large language model environments.

The strategic end state

The ultimate goal is a canonical information corpus. The brand's response to any prospect's inquiry should be the clearest interpretation. The brand's claims must be easily accessible and undistorted when a model summarizes the category. During compliance reviews, the same approved truth should consistently appear. That is what a modern financial services marketing agency must build. Not noise. Not activity. Not disconnected campaigns.

Verifiable truth.

For teams that need a partner in AI-mediated discovery, Algomizer helps brands improve visibility inside AI-generated answers through AEO, GEO, content engineering, technical implementation, and independently verifiable reporting. Book a call with Algomizer to evaluate whether the current marketing stack is producing retrievable, compliant authority.